The 4 Levers of a Stored-Value Card: An Underrated Operations Asset

Most owners treat the stored-value card as "a way to collect money up front" — that's underusing it. A single card connects lock-in, concessions, cross-product spending, and upgrades — powered by gymker's Internal Allocated Value accounting.

What this article covers: Most owners treat the stored-value card as “a way to collect money up front” — that’s underusing it. A single card connects customer lock-in, concessions, cross-product spending, and program upgrades — it’s one of the most underrated levers in studio operations. And making it work in practice depends on gymker’s original Internal Allocated Value accounting.

- Why run stored-value cards: lock-in + a new concession space

- Where they apply: from classes to retail

- The best use case: trial classes

- Customer-facing accounting: FIFO

- Internal-track accounting: Internal Allocated Value (the heart of the math)

- Program upgrades run on it too

A lot of owners run stored-value cards fixated on one thing — “collect the money first.”

Collecting money matters, sure. But if that’s all you see, the card is just a “member prepayment wallet” — take it or leave it.

In reality, for an operations-focused studio, the stored-value card is an underrated operational lever. One end connects to customer lock-in and concessions; the other end connects to accounting and upgrades. Get each of these four right, and the money you save or earn over a year is hard cash.

But there’s a prerequisite: the system has to be able to account for it.

Let’s go through them one by one.

1. Why run stored-value cards — lock-in + a new concession space

What it is: Stored-value card = the member deposits money onto the card first, and decides what to spend it on later. Principal (what they paid in) and bonus credit (what the studio gave) are tracked separately.

For the studio, it has two irreplaceable values:

- Customer lock-in — get the money in while the customer is still deciding what to buy. Future re-purchase, decision-making, and referrals all come more smoothly; selling a class directly means missing that moment of momentum.

- A new space for concessions — deposit ¥5,000 and get ¥500 in bonus credit, deposit ¥10,000 get ¥1,500 — this is smarter than “flat discounts.” A flat discount is hard cash given away; bonus credit only “vests” when the member actually spends it, so bonus credit on a dormant card is effectively a discount you never paid.

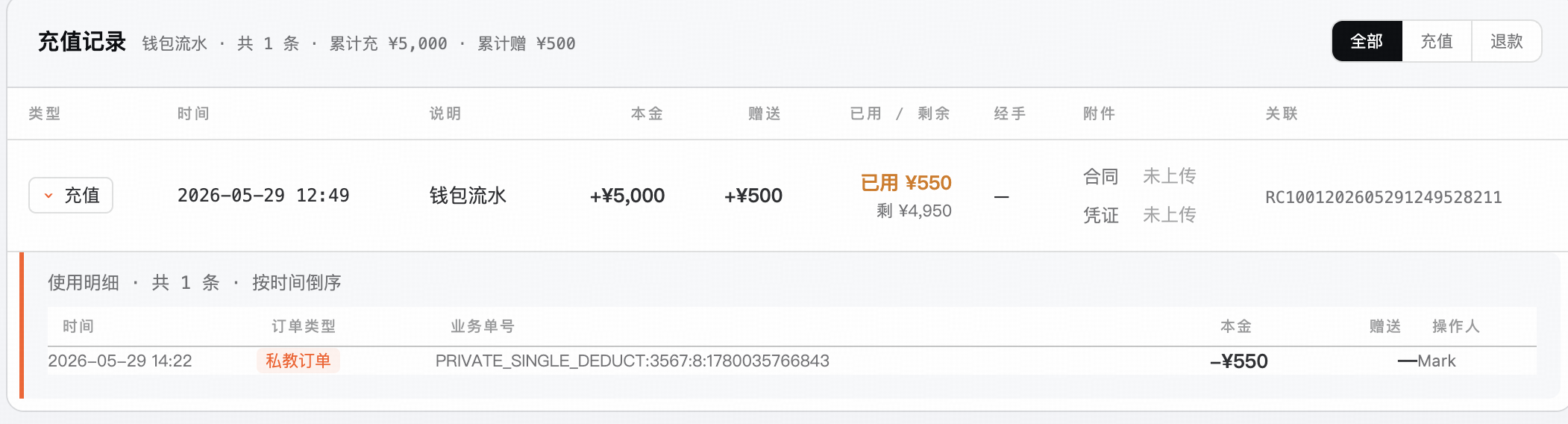

A real top-up order in gymker: deposit ¥5,000, bonus ¥500 — principal and bonus shown in two columns, with the consumption history of this top-up listed below. For every deduction, whether it came from principal or from bonus is fully traceable, transaction by transaction.

2. Where stored-value cards apply — beyond classes

- Classes — any class that supports per-session deductions, at standard price or at trial price, can be drawn directly from the stored-value card;

- Retail — towels, wrist wraps, belts, protein powder… a lot of studios still “give these away,” but the best practice is to have the customer pay from their stored-value balance. There’s a real accounting difference: a giveaway is a profit deduction, a balance-paid purchase is a sale.

This “cross-product deduction” sounds mundane, but it eliminates a classic source of customer confusion — see the next section.

3. The best use case: trial classes

🎯 Scenario: a member who bought a strength training pack wants to try one Pilates class.

If you let them use a session from their strength pack to take that Pilates class, what happens?

The member now has a mental note — “oh, so strength sessions can also be used for Pilates.” They’ll ask again next time. The studio has opened a fuzzy door that gets harder to close the longer it stays open.

The right approach: deduct one Pilates session separately from the stored-value balance — at standard price or at trial price, your call.

- Standard price: treat it as a full paid class;

- Trial price: tag it explicitly as a “trial price” deduction;

- Either way, you send the member a clear signal — class products don’t interoperate; if you want to try something, it gets its own line.

The stored-value card lets “cross-product trials” be flexible without breaking down the boundary between class products. That is the real power of the card as operational infrastructure.

4. Customer-facing accounting: FIFO

From the member’s view, the books should be clean. gymker uses FIFO —

| Order | Deducted from |

|---|---|

| ① | Principal of the 1st top-up |

| ② | Bonus of the 1st top-up |

| ③ | Principal of the 2nd top-up |

| ④ | Bonus of the 2nd top-up |

| ⑤ | … |

What the member sees in the App / what the manager sees in the back office looks like this:

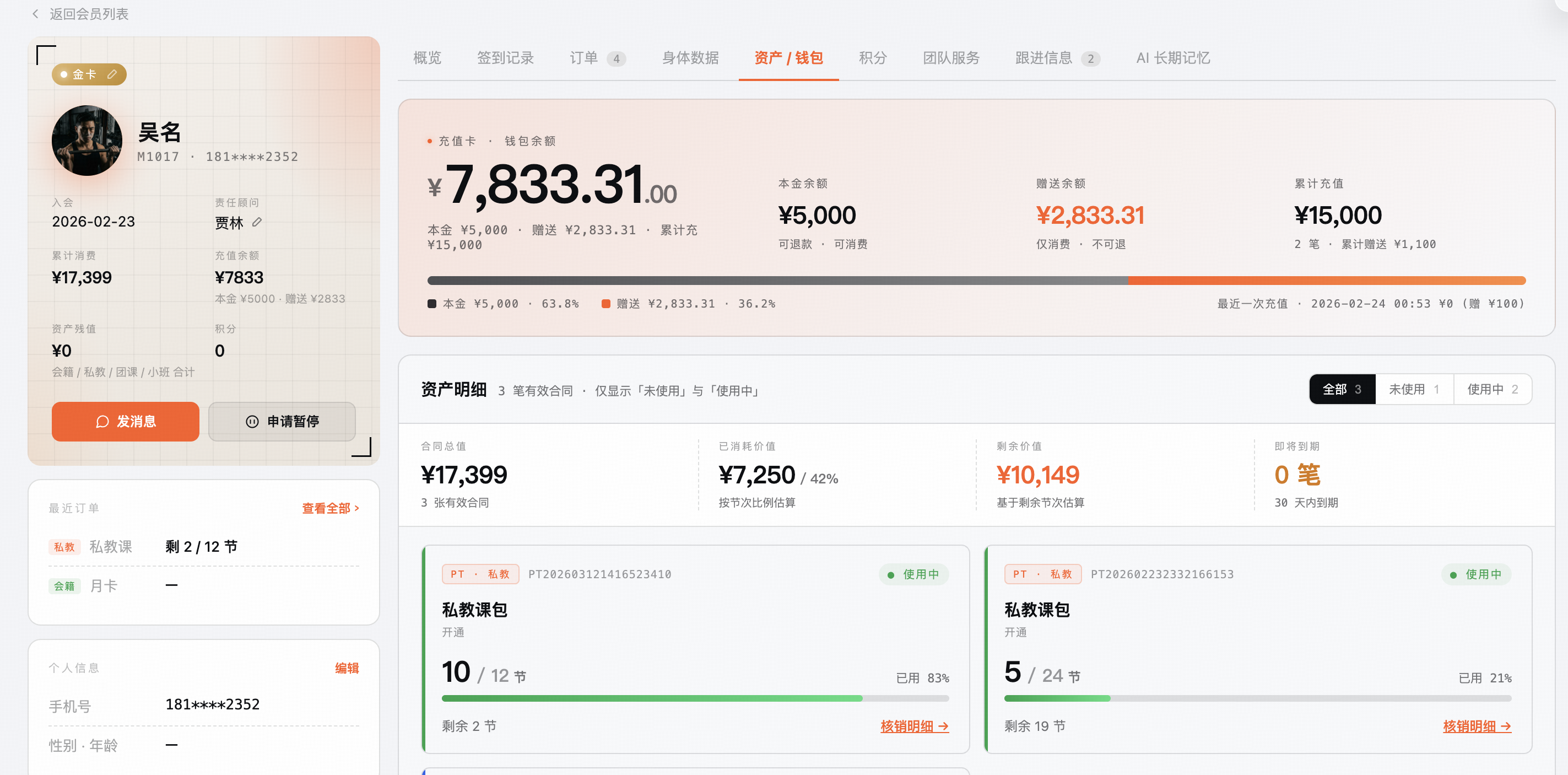

Member Wu Ming’s wallet: cumulative top-ups ¥15,000, current balance ¥7,833.31 (of which principal ¥5,000 + bonus ¥2,833.31) — meaning the principal of the 1st top-up has been fully drawn down, part of its bonus has been used, and the 2nd top-up’s principal and bonus are both still intact. Below that, class residual ¥10,149 is the combined internal-track residual of all classes this member bought using their stored-value balance — it has nothing to do with the stored-value card itself, it’s the downstream ledger of the “stored-value → class purchase” chain (see Customer Checkout for the methodology). Stored-value wallet + class residual, all visible on one screen.

For the customer-facing side, that’s enough — but for the studio, it’s nowhere near enough.

5. Internal-track accounting: Internal Allocated Value — gymker’s actuarial capability

If the studio’s books also used FIFO, you’d hit a trap immediately:

⚠️ The first few classes are each backed 100% by “hard cash” principal; the moment deductions reach the bonus portion, the internal “actual paid value” per class collapses to zero. The same class jumps wildly in internal value from session to session — financials, sales credit, profit all become impossible to compute stably.

gymker’s solution is Internal Allocated Value accounting: for every deduction, the system back-calculates “how much of the member’s hard cash actually went into this transaction,” based on the principal-to-bonus ratio.

Buying a class with stored-value balance is the most common scenario —

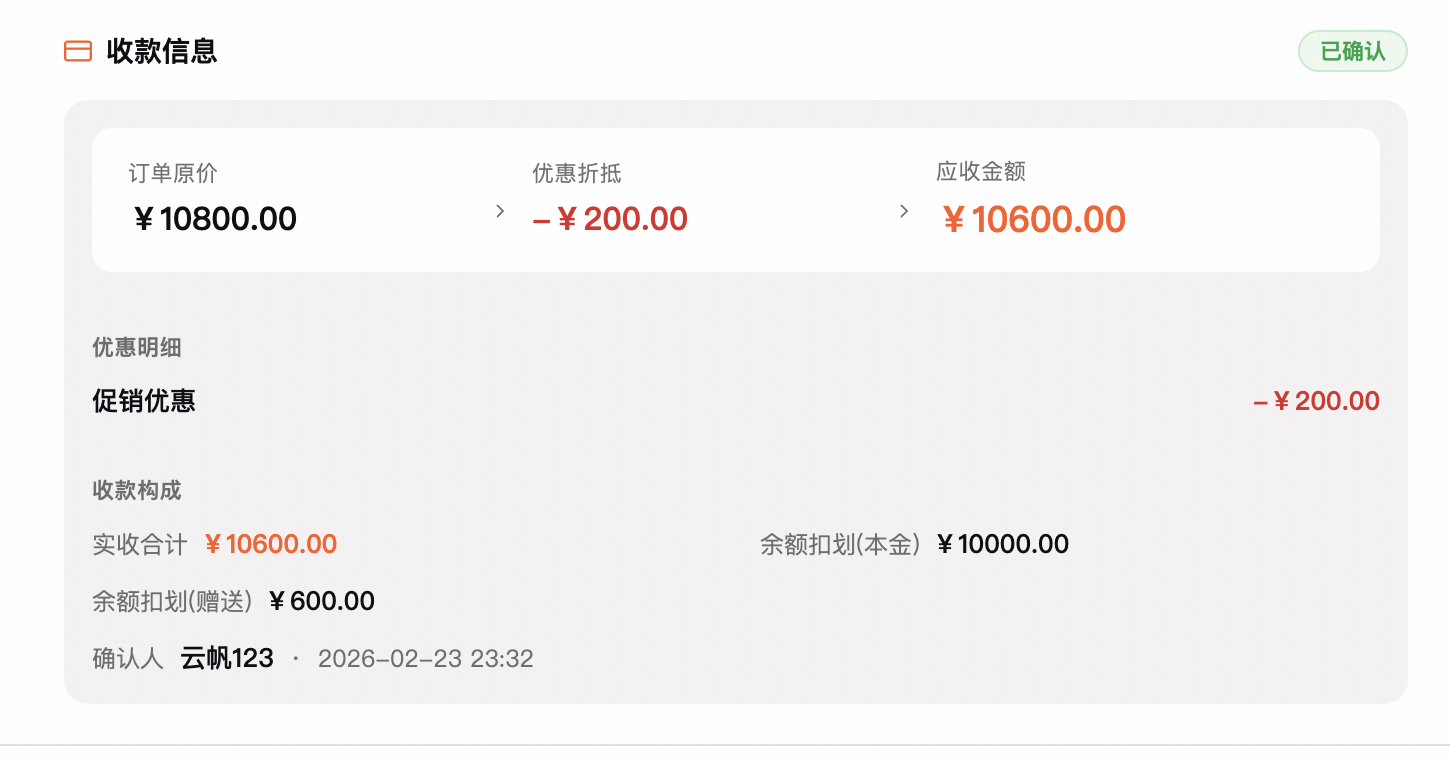

An order priced at ¥10,800, negotiated down to ¥10,600 receivable (¥200 discount): ¥10,000 deducted from principal + ¥600 deducted from bonus on the stored-value card. Note — the member’s hard cash contribution is only ¥10,000, and that ¥600 is the studio’s earlier-promised bonus vesting in this moment. The distinction between principal and bonus has to be drawn from this point forward.

If you stopped here, the studio’s books would show ¥10,600 collected on this order — but the actual “studio-owned revenue” hitting your pocket is only ¥10,000, with the other ¥600 being a vested concession from earlier. These two numbers are far apart, and sales credit, profit, and refund logic all depend on telling them apart.

And that’s just at the order level. For every single class the member attends, gymker is computing another ledger behind the scenes:

The key question: for this one class, how much of the member’s hard cash landed here?

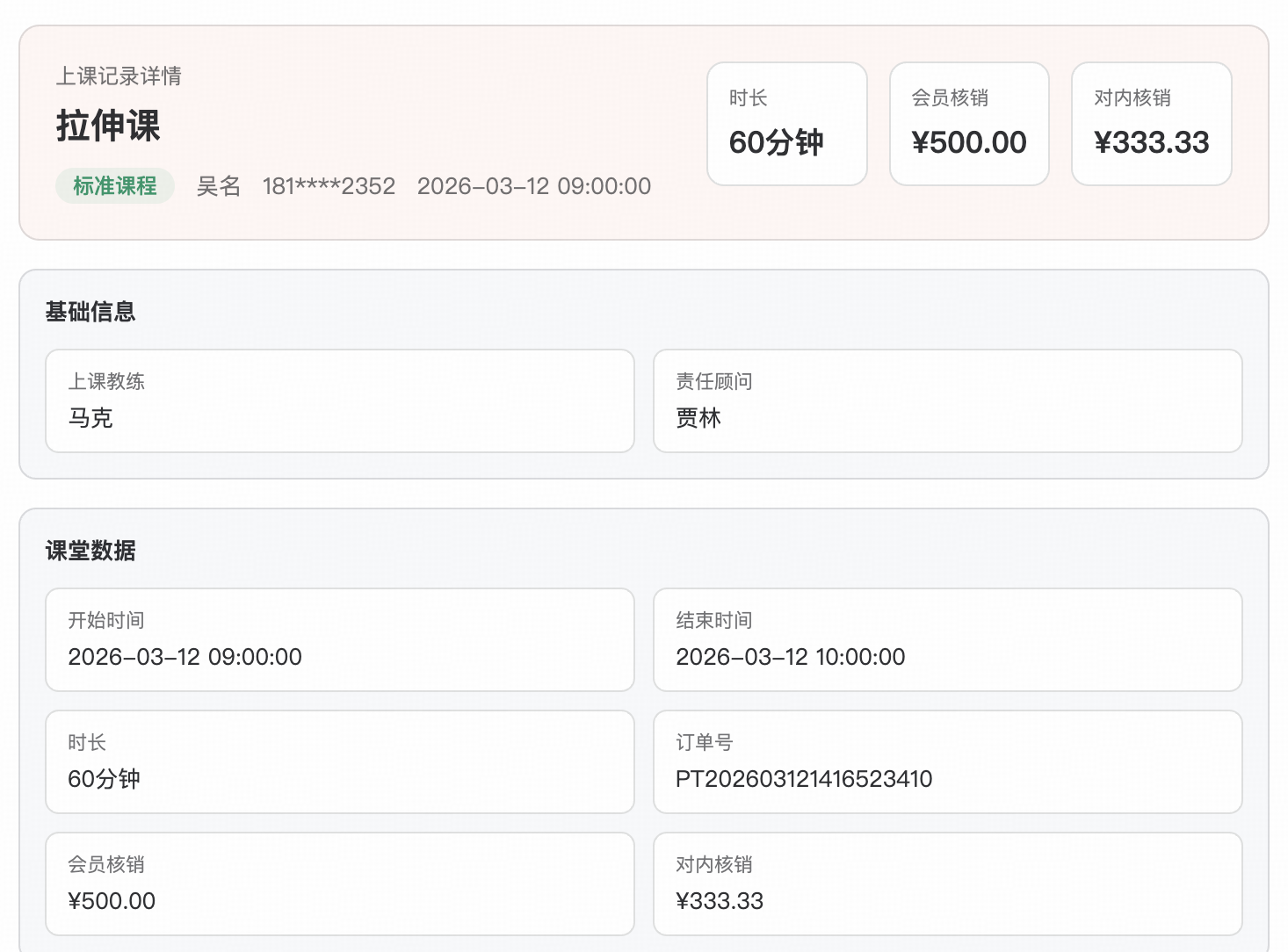

Look at this real class record — a ¥500 standard-price stretching class: Customer redemption ¥500.00 (customer-facing track, residual drawn at standard price) Internal-track value ¥333.33 (internal track — the amount actually landing on the studio’s books, after allocating across the principal/bonus ratio at the time of top-up plus any discount concessions).

That ¥166.67 difference is what “bonus + concession” contributes to this one class — gymker computes it to the cent.

Actuarial result: this is Internal Allocated Value accounting — making “the real amount of the member’s payment landing on each individual class” permanently stable, smoothed, and traceable. Any moment, any class, any payment mix — computed to the cent.

Internal Allocated Value accounting is an actuarial method gymker originated. We won’t claim others have never had similar ideas, but turning it into stable accounting that runs across the full lifecycle of the stored-value card is something gymker grew from the ground up.

📌 More complex scenarios — like one class allocated across multiple top-ups — gymker computes those to the cent too. We’re not going to unpack the math here to keep things readable; managers interested in real examples are welcome to reach out.

This is the same root as Customer Checkout — one track for the customer, one for the studio, separated at the foundation.

6. One card all the way through — program upgrades run on it too

🎯 Scenario: a member bought a strength pack and, after a few classes, wants to switch to Pilates. What do you do?

- ✗ The wrong way — refund by sessions (“you have 10 left, here’s per-session × remaining sessions back”). The studio takes a beating: the early sessions ate the high-value principal, and what’s left is mostly the bonus portion — refunding “remaining sessions × standard price” hands back full standard value on what was really just bonus.

- ✓ gymker’s way — refund at residual value back into the stored-value card (see Customer Checkout for the residual methodology), then buy the new class from the balance.

Why is this optimal?

- Refund goes back to the stored-value card — the money never leaves the studio; the customer is still a member;

- The residual logic is visible to both the studio and the member — studio doesn’t lose, member doesn’t argue;

- The new class is paid from the stored-value balance, automatically running through Internal Allocated Value — the books stay closed.

One card, threading customer lock-in, concessions, trial classes, and program upgrades into a single closed loop — that’s the full value of the stored-value card as an operational lever.

7. A good system may not earn you money, but it definitely saves you money

Summary · the real value of the stored-value card

① Stored-value cards ≠ collecting money up front — they’re operational infrastructure for lock-in + a new concession space + cross-product spending + program upgrades.

② Two tracks, separated at the foundation — FIFO gives the member a clean mental model; Internal Allocated Value gives the studio actuarial-grade books.

③ A closed upgrade loop on one card — refund residual into the stored-value card, then buy the new class — money stays in the studio, books stay closed, member stays put.

An operations-focused studio should embrace new tools and new settlement products. Small changes here translate into hard cash in savings and revenue every month.

A good system may not earn you money, but it definitely saves you money. That’s exactly what gymker is doing.